Feeling the pressure of the upcoming tax deadline? The stress of gathering documents and fearing missed deductions is a common burden for many Inland Empire residents.

Fortunately, a clear and comprehensive tax preparation checklist can transform this anxiety into confidence. With expert guidance from Catalyst CPA experts, you can navigate tax season smoothly and maximize your financial outcome.

Essential Takeaways

- Crucial: Systematically organize your personal, income, and expense documents to prevent costly errors.

- Subsequently, implement strategic year-end moves like maximizing retirement contributions to lower your taxable income.

- Partnering with a professional CPA ensures you capitalize on every available deduction and credit.

Essential Document Tax Preparation Checklist

First, gather your foundational personal information. This ensures accuracy from the very start. It is the first step in any tax preparation checklist.

- Critical: Social Security or ITIN numbers for yourself, your spouse, and all dependents.

- Critical: Bank account and routing numbers for direct deposit of your refund.

- Critical: A copy of last year’s federal and state tax returns for reference.

- Critical: Any Identity Protection PINs issued by the IRS for family members.

Crucial Income & Investment Documentation

Next, you must report all sources of income. The IRS requires detailed records of earnings. This prevents future audits and penalties.

What forms do I need for employment income?

Gather all statements related to your job. This includes traditional and freelance work. Each form reports different income types.

- Forms W-2: From every employer you worked for during the year.

- Forms 1099-NEC/MISC: For any freelance, contract, or miscellaneous income.

- Forms 1099-R: For distributions from retirement plans like a 401(k) or pension.

- SSA-1099: For any Social Security benefits you may have received.

What about investment and other income sources?

Investment income is also critically important. This includes interest, dividends, and stock sales. Accurate reporting is essential for compliance.

- Forms 1099-INT/DIV/B: For interest, dividends, and brokerage transactions.

- Schedule K-1: For income from partnerships, S-corps, or trusts.

- Rental Income Records: Including all associated expenses and depreciation schedules.

Ready to Transform Your Tax Strategy?

Maximize Your Return: Deductions & Credits

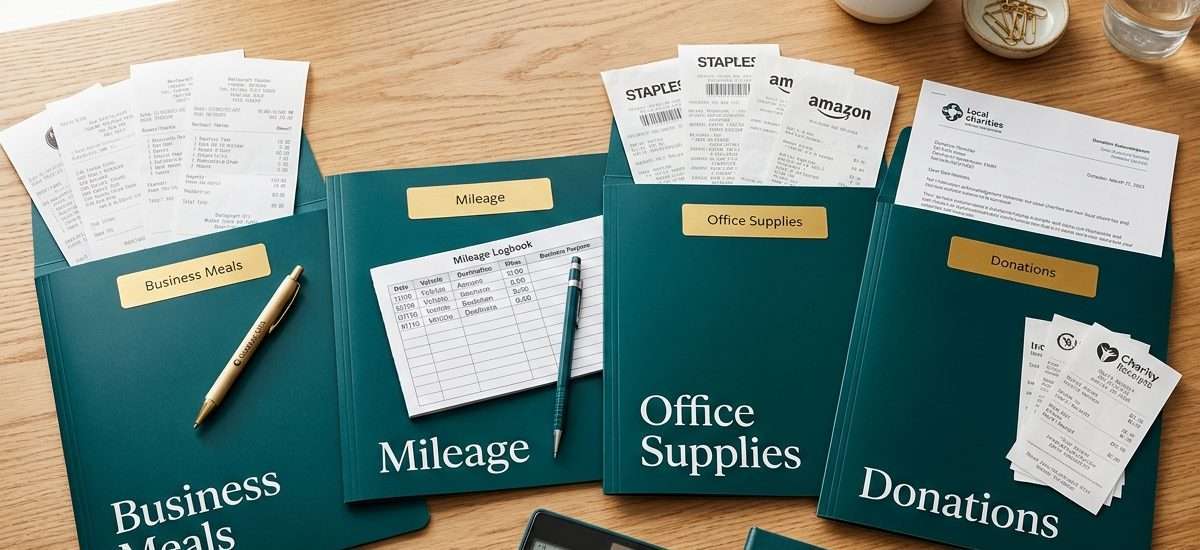

Finally, collect all documents for potential deductions. This is where you can significantly lower your tax liability. Attention to detail is key here.

- First, gather homeownership documents. This includes Form 1098 for mortgage interest and property tax records.

- Second, compile medical expense records. Include health insurance premiums and out-of-pocket costs.

- Third, find charitable contribution receipts. This applies to both cash and non-cash donations.

- Fourth, organize educational expenses. Collect Form 1098-T for tuition and 1098-E for student loan interest.

Critical Alert: The IRS requires robust documentation for business expenses. Keep detailed logs for home office use, vehicle mileage, and all receipts to substantiate your deductions. Failure to do so can result in disallowed expenses during an audit.

Strategic Year-End Tax Saving Moves

Even late in the year, you have opportunities. You can take action to reduce your 2024 tax bill. Consider these powerful strategies.

| Strategy | Key Benefit |

|---|---|

| Maximize Retirement Contributions | Reduce your taxable income dollar-for-dollar. You have until April 15, 2025, for IRA contributions. |

| Tax-Loss Harvesting | Sell losing investments to offset capital gains and potentially deduct up to $3,000 against other income. |

| Charitable Donations | If you itemize, donations made before Dec 31 can provide a valuable deduction. |

Essential Questions About Tax Preparation

What if I cannot pay my tax bill by the deadline?

First and foremost, you should still file your return on time. The failure-to-file penalty is much higher than the failure-to-pay penalty. You can then explore IRS payment options like an installment agreement.

How long should I keep my tax records?

Generally, the IRS has three years to audit a return. However, we strongly recommend keeping all tax records for at least seven years. It is always better to be safe and organized. You can learn more at the California Franchise Tax Board website.

Do I need a professional if my taxes seem simple?

Even simple returns can hide opportunities. A professional CPA can identify overlooked credits and deductions. Therefore, professional help often pays for itself. You can schedule your free consultation to see how we can help.

Ready to Revolutionize Your Financial Future?

Discover how Catalyst CPA transforms your success.

About Catalyst CPA

We’re the catalyst for your financial transformation. Moreover, our certified experts deliver personalized strategies. Therefore, you achieve remarkable results.

Important Notice: This content provides general information only. Furthermore, tax laws evolve constantly. Therefore, consult our qualified CPAs for personalized guidance. Review our privacy policy for details.

Catalyst CPA Newsletter

Get 2026 tax-saving tips in your inbox

Real, CPA-written guidance for Inland Empire small businesses — bookkeeping, tax planning, IRS updates. No spam, unsubscribe anytime.

By subscribing you agree to receive emails from Catalyst CPA. We never share your email. Unsubscribe with one click anytime. Questions? Call (951) 223-1826.